Description

Introduction to Internal Controls

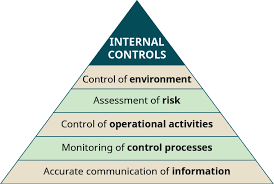

Internal controls are essential mechanisms that organizations implement to ensure the integrity of financial and operational processes. These controls help mitigate risks, ensure compliance with laws, and enhance the efficiency of operations.

Preventive Controls

Preventive controls are designed to deter errors or fraud before they occur. Examples include segregation of duties, proper authorization of transactions, and comprehensive training programs for employees.

Detective Controls

Detective controls aim to identify errors or irregularities that have already transpired. Regular audits, reconciliations, and inventory counts fall under this category, ensuring any discrepancies are promptly discovered and addressed.

Corrective Controls

Corrective controls are measures implemented to rectify issues identified by detective controls. These may involve updating policies, revising procedures, and conducting follow-up audits to ensure problems are resolved and prevented from reoccurring.

Lovie –

casino la roche posay

References:

https://bookmark4you.win/story.php?title=win-at-〔progressive-jackpot-slots〕-in-2026-australia

Laverne –

poker bonus no deposit

References:

https://latenews.top/item/484189

Hollis –

steroids side effects on males

References:

pattern-wiki.win

Clint –

androgenic effects

References:

wolfe-forrest-2.mdwrite.net

Jerry –

References:

Skycrown casino table games

References:

https://graph.org/Top-Australian-Online-Casino-Sites-2026-04-20

Dotty –

References:

Casino 777 be

References:

https://graph.org/Casino-Online-Best-Sites-Games–Bonuses-04-20

Vernell –

References:

Comanche red river casino

References:

https://casino-singapore.online-spielhallen.de/

Drusilla –

References:

Branson mo casinos

References:

https://gzuz-casino.online-spielhallen.de/

Brock –

References:

Gelsenkirchen

References:

https://borengo-casino.online-spielhallen.de/

Teddy –

References:

Würzburg

References:

https://candy-casino.online-spielhallen.de/

Chong –

References:

Berlin

References:

https://casino-blankenberge.online-spielhallen.de/

Ila –

References:

Göttingen

References:

https://wo-ist-das-casino-in-gta-5.online-spielhallen.de/

Kristi –

References:

Indio casino

References:

https://graph.org/Does-Newcastle-Have-A-Casino-04-27